")

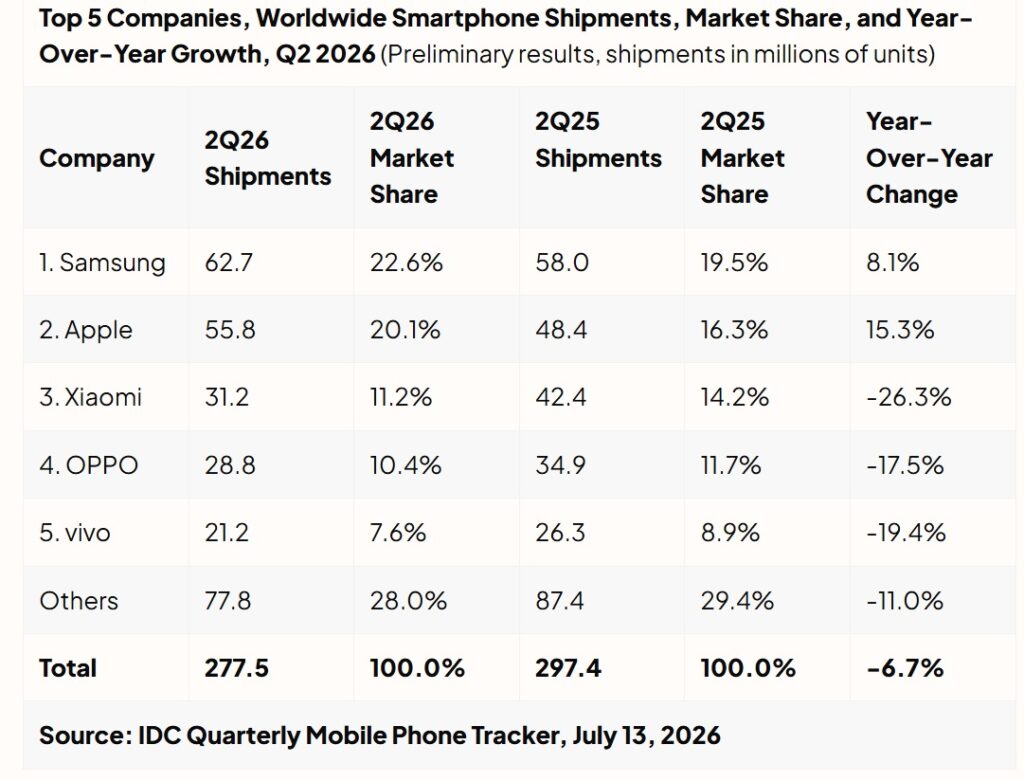

Global smartphone shipments fell 6.7% year on year in the second quarter of 2026 as soaring memory costs hit manufacturers of low-priced devices harder than premium brands, according to preliminary data from research firm IDC.

Shipments dropped to 277.5 million units during the quarter, marking the market’s second consecutive year-on-year decline.

IDC said memory costs have increased by nearly 300% from a year earlier and now account for more than 65% of the bill of materials for some entry-level smartphones.

The cost pressure has forced vendors reliant on inexpensive, high-volume devices to reduce shipments, reuse older models, or offer more 4G variants.

“Memory costs are up nearly 300% from a year ago, and now account for over 65% of BOM at the low end, making survival increasingly difficult for OEMs with low-end portfolios,” said Nabila Popal, senior research director for Worldwide Consumer Devices at IDC.

“This is not a uniform downturn; memory crisis is favoring premium players and punishing vendors exposed to the low end,” she added.

Samsung and Apple were the only companies among the five largest smartphone vendors to record shipment growth during the quarter. Their global market shares rose by 3.2 percentage points and 3.8 percentage points, respectively.

Apple posted record second-quarter shipments, driven by demand for the iPhone 17 and consumer concerns over possible price increases, according to IDC. The research firm expects Apple to secure a record 22% share of annual smartphone shipments in 2026.

“This memory crisis has split the smartphone market in two,” said Francisco Jeronimo, vice president for Worldwide Client Devices at IDC.

“At the top, Apple and Samsung are pulling away, because they secured supply early and sell where memory is a smaller share of the bill of materials (BOM). At the bottom, the vendors exposed to cheap, high-volume devices are absorbing the pain and so are their customers.”

Jeronimo said the shortage favors companies with greater scale, stronger supply relationships, and a larger share of premium devices in their product portfolios.

Xiaomi, Oppo, and vivo retained their rankings from the previous quarter, but IDC said shipment declines among Chinese smartphone companies accelerated, with most major vendors posting double-digit contractions.

The sub-$200 segment remains an important source of volume for these brands. Some vendors have responded by repackaging older devices or releasing 4G models to control costs and maintain their presence in the segment.

Xiaomi recorded the steepest decline among the market’s largest vendors as it deliberately reduced low-end shipments to protect profitability and focused on more expensive devices.

Huawei bucked the trend, posting 20.9% year-on-year growth. IDC attributed the increase to stable pricing, targeted promotions, strong brand loyalty in China, and a broader product lineup.

“Consumers are increasingly opting for a premium brand when the price gap reduces, and financing is readily available,” Popal said.